If they have the cash easily accessible to possess a deposit, they may be able go the standard route through getting a fixed- or changeable-rate mortgage.

If they do not have the finance but have equity collected in their home, capable thought a home equity line of credit (HELOC).

It is one good way to make use of the debt equity you’d has actually inside the a property, shows you Aneta Zimnicki, home loan agent from the Dominion Financing Centres in Toronto. If you possess the correct money vehicles you to definitely yields output high than the cost of borrowing, it is an approach to dedicate without having to basically fool around with all of your funds (come across Dangers of credit to spend on the our very own tablet version.)

Here’s how it works: a HELOC is a protected credit line up against your existing possessions. Which means the lending company could offer you a much lower rates because of the equity, says Zimnicki. Often the price try prime and another, otherwise best and additionally 50 % of, with respect to the bank.

Therefore a customer may take away an effective HELOC up against her first home, including, and make use of those funds while the a downpayment for an investment possessions. And there is an income tax work with if you are using the amount of money off a HELOC to expend, same as if you use home financing to spend. In the two cases, the borrowed funds focus are tax deductible.

So share with website subscribers to trace how they use the HELOC if the the whole number isn’t really useful investment intentions. In the event the an individual uses ten% of your own HELOC purchasing an ice box, for instance, after that that comes around individual fool around with and you can 10% of one’s focus is not tax deductible.

Extremely HELOCs into the Canada enjoys a long label. Thus, clients are toward link having notice just, states Amy Dietz-Graham, investment coach within BMO Nesbitt Injury during the Toronto. In addition to line of credit are discover, therefore a person takes away currency, lower and take out once again in the place of penalty (get a hold of Definite or long?).

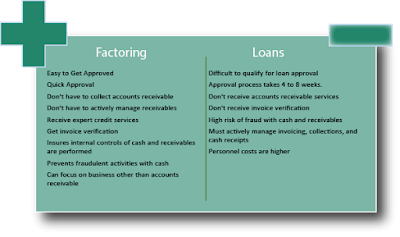

To own a mortgage, the customer has actually a flat fee monthly based on desire along with dominating. And you will, when the an individual pays a home loan till the label are up, she’s subject to punishment.

But there is however a threat having HELOCs. Because they are according to rates, payment wide variety can be change. The danger is similar to changeable-price mortgage loans, that can rely on interest rates (discover Home loan against. HELOC).

You ought to be available to that and make certain you have had adequate cash on hand so you’re not in times where you’re not able to make the money, warns Dietz-Graham.

David Stafford, managing director of A home Shielded Credit from the Scotiabank into the Toronto, cards that because there is notice-rate risk, its restricted. State a consumer removes an excellent $100,000 credit line, therefore the Lender off Canada actions cost upwards 0.25%. One quarter area will definitely cost a client from the $20 more a month. That have that percentage go up by $20 is not going to materially feeling anyone’s cashflow. Costs would have to take action most in love to be a great situation.

But, whether your client is actually leveraged with numerous HELOCs towards multiple features, up coming she is in some trouble when the cost rise. And while HELOCs are always claimed in order to credit bureaus, sometimes mortgage loans are not (generally speaking when your financial is by using a smaller sized financial). Therefore if a client misses a repayment on the a beneficial HELOC, Dietz-Graham says it is more likely one including a mistake is also harm their own credit rating, compared to the a missed mortgage payment.

Financial compared to. HELOC

Zimnicki contributes advisors should begin the fresh new discussion on whether or not to need out a beneficial HELOC having money objectives which have customers very early, especially since they is generally installment loans Florida prone to get approved to have one to ahead of they have numerous characteristics.

Ask for money when you do not require they, she advises. When someone claims, I have burned up all my personal bucks, now I would like to make use of my personal house guarantee,’ possibly this may takes place. But a finest configurations most likely might have happened prior to in the [the newest consumer’s] portfolio.

Putting a HELOC to work

A good HELOC can be used to put money into automobile beyond property. Certainly one of Dietz-Graham’s customers did exactly that. The customer got paid the borrowed funds towards the his $2-mil primary household and you can decided to sign up for a HELOC. He borrowed $100,000 to spend solely in the companies.

Due to the fact rates are so reasonable, they offered your the ability to put money into highest-high quality businesses that were using highest dividends than what the interest rate is, says Dietz-Graham.

Given the buyer’s web value, the amount he borrowed are suitable and he fully knows the new risks of playing with borrowed finance getting spending, because it is not a technique for someone.

Specified or long?

According to Monetary Individual Agency of Canada, there are two sorts of HELOCs. You to boasts a definite label, and therefore an individual needs to repay it within the complete by a predetermined go out (five so you can twenty five years, depending on the bank). The full time up until the HELOC grows up is named the fresh mark several months, during which a person can be withdraw around the utmost borrowing restriction and simply must spend the money for attention. If the she will pay along the HELOC, she can withdraw again before the maturity day.

not, most Canadian loan providers provide HELOCs having long terms and conditions. Exactly like credit cards, they are available having revolving borrowing as there are no maturity day. Once again, money arrive as much as the absolute most the client could have been accepted having.

Very, an individual can acquire, lower and you will acquire again indefinitely. Although the client is just needed to pay the attract each month, if the she will pay down prominent, that can opened investment so you can reinvest.

For instance, state a client possess paid down the mortgage on her $400,000 number 1 house. Playing with an excellent HELOC having an indefinite label, she borrows as much as the utmost 65% out-of their own house’s appraised worthy of-$260,000-and you may spends the entire matter into the accommodations possessions. Once three years, this woman is made use of the productivity on leasing to spend down their HELOC, so she’s an identical $260,000 accessible to purchase a 3rd property.